🚀 Bpifrance’s International Expansion Insurance: The Expert Guide to Financing and Securing Your International Expansion

Bpifrance’s Market Development Insurance (AP) has become a go-to option for many French SMEs seeking to accelerate their international expansion. On paper, the program is attractive: it finances a significant portion of export prospecting expenses while limiting the risk of commercial failure. In practice, however, if poorly calibrated or managed in silos, AP can turn into a financial and operational trap that weighs on margins and cash flow.

To ensure it serves as a genuine FinOps export tool—rather than a “magic” grant whose true cost only becomes apparent years later—it is essential to fully understand how it works, grasp the repayment mechanisms, and integrate it into an overarching framework for financing international development.

A hybrid mechanism combining cash advances and risk sharing

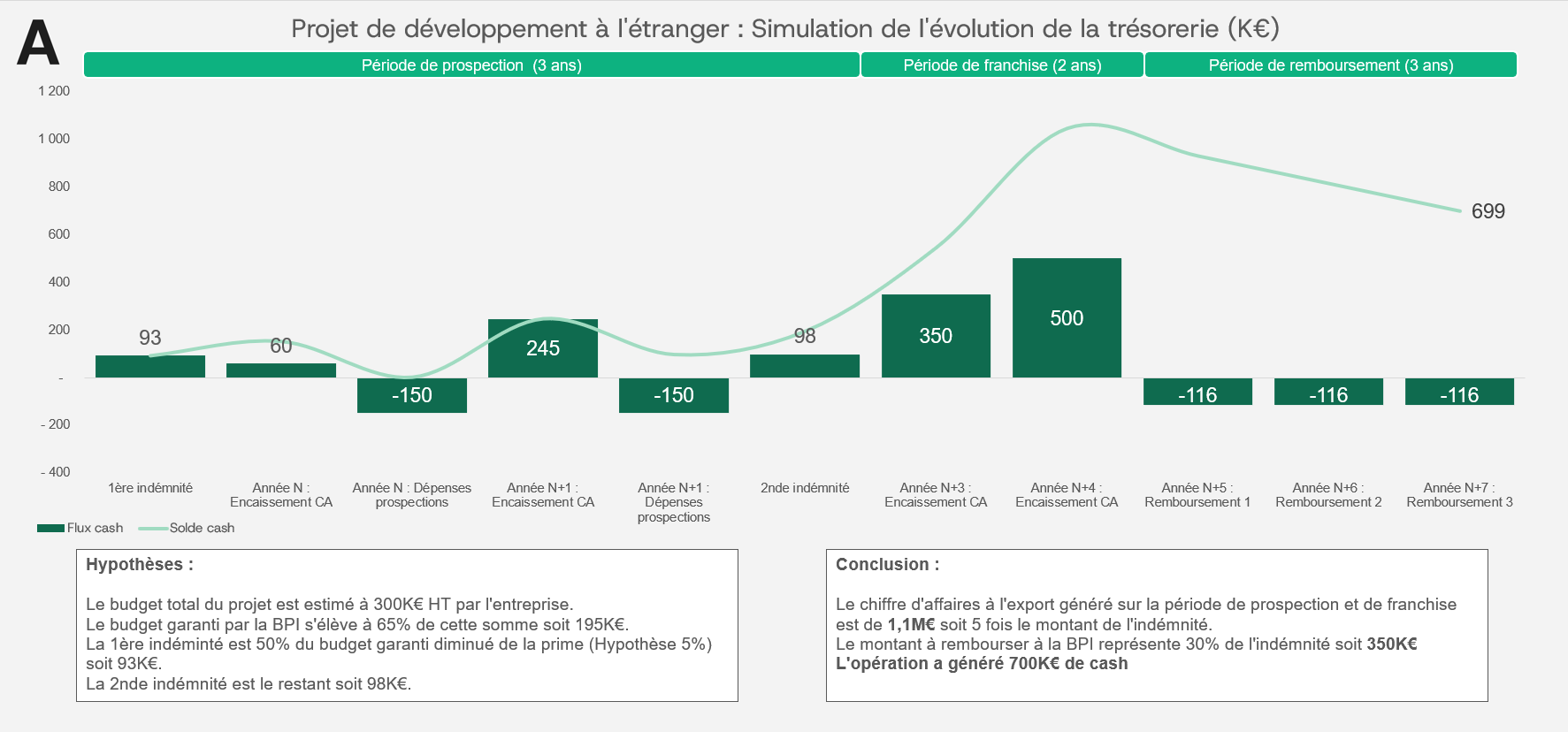

The Exploration Insurance Program is a hybrid mechanism combining elements of both a grant and a loan. The program covers up to 65% of exploration expenses in a given geographic area over a 7- to 9-year cycle.

The cycle consists of three phases. The prospecting phase (2–3 years): the company initiates its activities. The franchise phase (2 years): no reimbursement; initial results should begin to appear. The reimbursement phase (3–4 years): the company returns all or part of the compensation based on the export revenue generated.

The strength of this system lies in its hybrid nature. Complete success: full reimbursement. Partial success: reimbursement indexed at 10% of export revenue. Failure: a minimum lump-sum payment of approximately 30% of the compensation. The risk appears limited, but this model is effective only if the budget, revenue trajectory, and internal organization are properly aligned from the outset.

The Three Faces of the Financial Trap

The first risk: an oversized budget. Public relations budgets range from a few tens of thousands to several hundred thousand euros. There is a strong temptation to aim for the upper end of the range. But an oversized budget creates a windfall effect: spending skyrockets on “cosmetic” initiatives (communications, events, travel) without a foundation of recurring revenue. When it comes time to repay the loan, the drain on margins and cash flow becomes significant relative to the results achieved.

The second challenge concerns the traceability of export revenue. The AP relies on a clear correlation between spending and export revenue generated in the region. This correlation becomes more complex when sales flows go through distributors, marketplaces, or subsidiaries. Without granular export reporting (by region, channel, and customer), the company struggles to demonstrate the impact of its spending. It must then accept an unfavorable flat-rate reimbursement or heavily involve its finance and sales teams in time-consuming administrative work.

The third risk is administrative overload. The AP requires proof of eligibility for expenses, documentation of the “French share” (at least 20% of value added created in France), and the retention of all supporting documents. For an SME without a dedicated export finance team, this documentation requirement represents a significant hidden cost. The time spent gathering documents and justifying allocations can quickly erode the benefits of the program.

From Acquisition to Revenue: Integrating AP with a Comprehensive FinOps Strategy

Sales Prospecting Insurance should not be viewed as a standalone tool focused solely on acquiring new customers. It addresses the risk of the investment failing to generate revenue—but leaves the risk of non-payment and the working capital requirements associated with orders unaffected.

A mature approach involves integrating it into a comprehensive export financing chain, coordinated with trade finance tools. The AP pre-finances market development activities (trade shows, business missions, product adaptation, marketing, and recruitment). Downstream, the Letter of Credit (LC) andthe UPAS ensure execution and payment terms. The LC facilitates payment through the buyer’s bank, while the UPAS offers the customer payment terms while guaranteeing cash collection through the bank.

By combining these components, the company funds its expansion and ensures payment collection. The AP becomes the cornerstone of an export FinOps architecture that covers the entire process, from market research to invoice collection.

Optimize the parameters: duration, French share, and operational management

Value lies in the configuration and management. The length of the sales cycle is a key factor. For short cycles (SaaS, digital acquisition), two years are sufficient. For manufacturing, infrastructure, or healthcare, three years are often needed to convert leads and generate export revenue.

The French component is a strategic factor, not merely a constraint. Documenting precisely where value is created in France (R&D, production, engineering, support, logistics) strengthens the case and facilitates audits. It also clarifies the value chain, which is useful when dealing with banks and investors.

Success depends on proactive management: tagging eligible expenses as soon as they are recorded in the ERP system, organizing a cost-accounting system by region, and synchronizing the schedule with reporting deadlines. A simple governance structure (a finance-sales partnership) makes it possible to anticipate bottlenecks and transform the AP into a performance contract.

Conclusion: A barometer of FinOps maturity

Prospecting Insurance reveals the level of FinOps maturity in a company expanding internationally. If not properly managed, it becomes a burden: refunds that eat into margins, administrative overhead, and insufficient tracking of export revenue.

As part of a comprehensive financing framework that incorporates trade finance tools and robust governance, the AP serves as a powerful risk buffer. It enables companies to test new markets, finance export investments without straining cash flow, and establish reporting structures that enhance the company’s credibility.

The Prospecting Insurance Program is not merely a public support tool: it serves as a test of consistency between international ambitions, the soundness of the export business plan, the quality of information systems, and the ability to execute a profitable and well-managed growth strategy.